/* Debug: Make toggle content visible */

.pafe-toggle-content {

border: 2px solid red !important;

min-height: 30px !important;

}

/* Debug: Show full content on hover to verify it's there */

.pafe-toggle-content:hover {

height: auto !important;

}

Skip to content

Medaro Mining Corp. is a Canadian mineral exploration company dedicated to building a secure supply of the minerals critical for energy, and high‑tech applications.

Critical minerals underpin industries worth trillions of dollars.[1]

Their value is a direct consequence of growing demand…

They are essential to economic or national security functions (energy systems, defense, high‑tech manufacturing).

Supply chain vulnerability impacted by disruption (high import reliance, concentrated foreign production, geopolitical risk, or by‑product dependence).

If disrupted, the impact can cause significant economic damage or national security risk.

Precious metals have experienced an unprecedented, historic, and record-breaking rally, with gold surpassing $5,000 per ounce in early 2026 and some forecasting $6,000 this year. This bull market has seen the sector transition from a hedge into a major, high-performing asset class.[2]

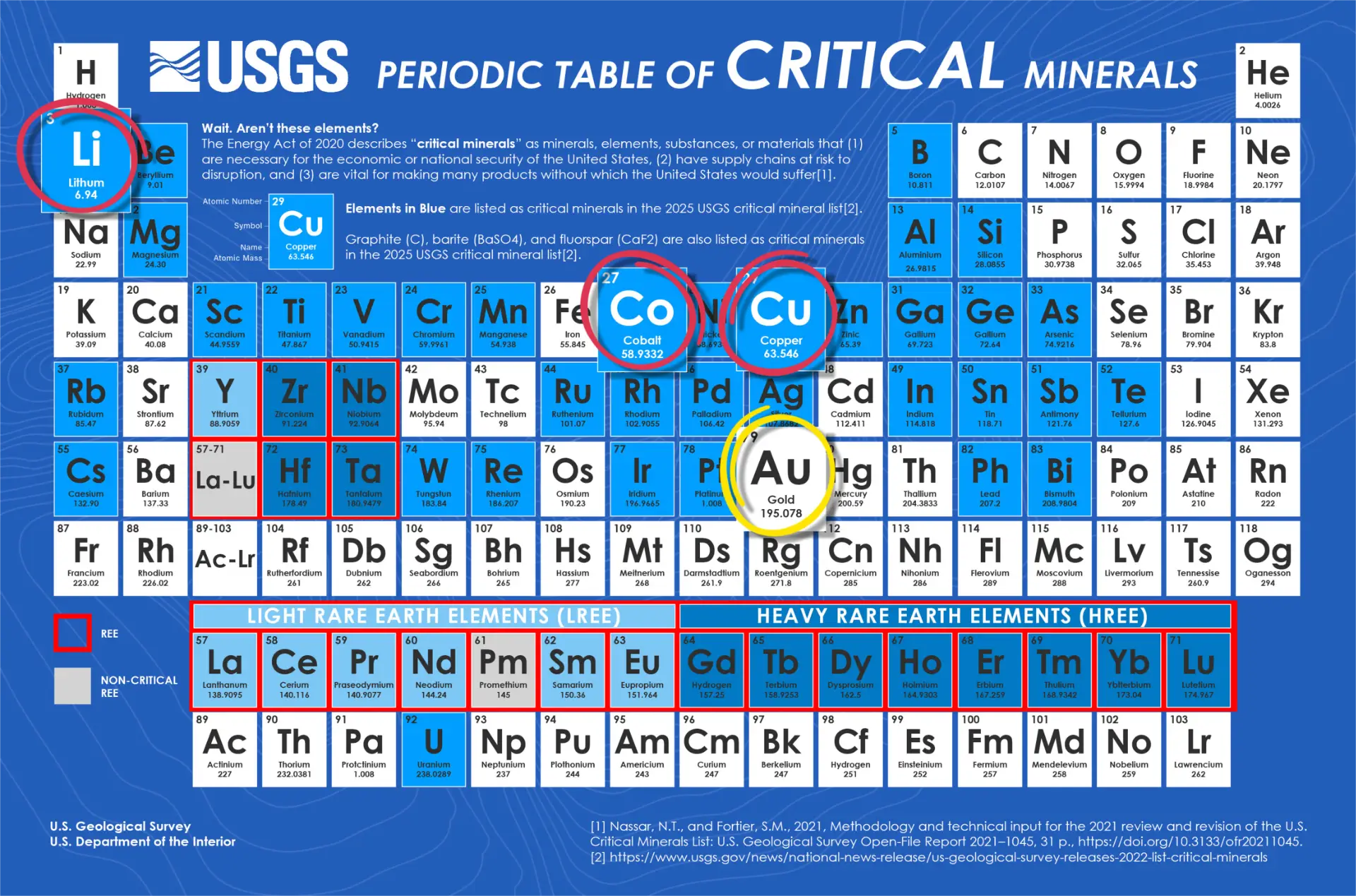

Medaro Mining’s opportunity targets highlighted in RED and YELLOW above.

RARE EARTH ELEMENTS: CRITICAL DEMAND

REEs

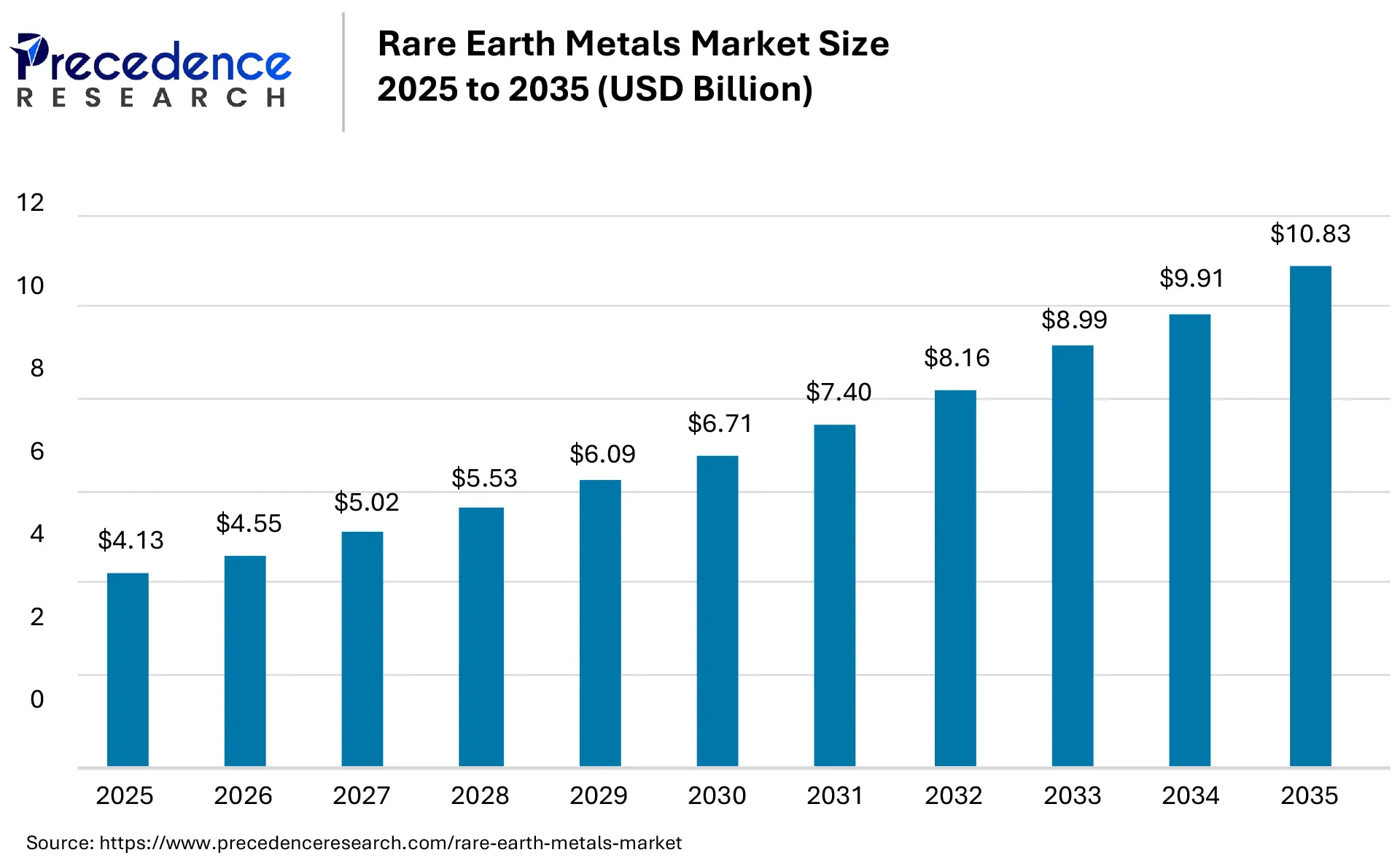

The global Rare Earth Metals market size is accounted at USD 4.13 billion in 2025 and predicted to increase to approximately USD 10.83 billion by 2035. The rising demand for EV’s, renewable energy, data centers, and the smart technologies, which require permanent magnets, are the major driving factors of the market.1

According to the IEA China accounted for about 70% of global rare-earth extraction in 2024 and controls more than 90% of the downstream value chain, including refining, and magnet production.2

Now Western governments are creating renewed domestic rare earth demand with industrial policy aimed at breaking China’s long held supply chain stranglehold. The U.S. Department of Defense is explicitly funding rare-earth mine‑to‑magnet chains for advanced missiles, sensors, fighter jets, Navy ships and other platforms dependent on permanent magnets and specialty alloys.2

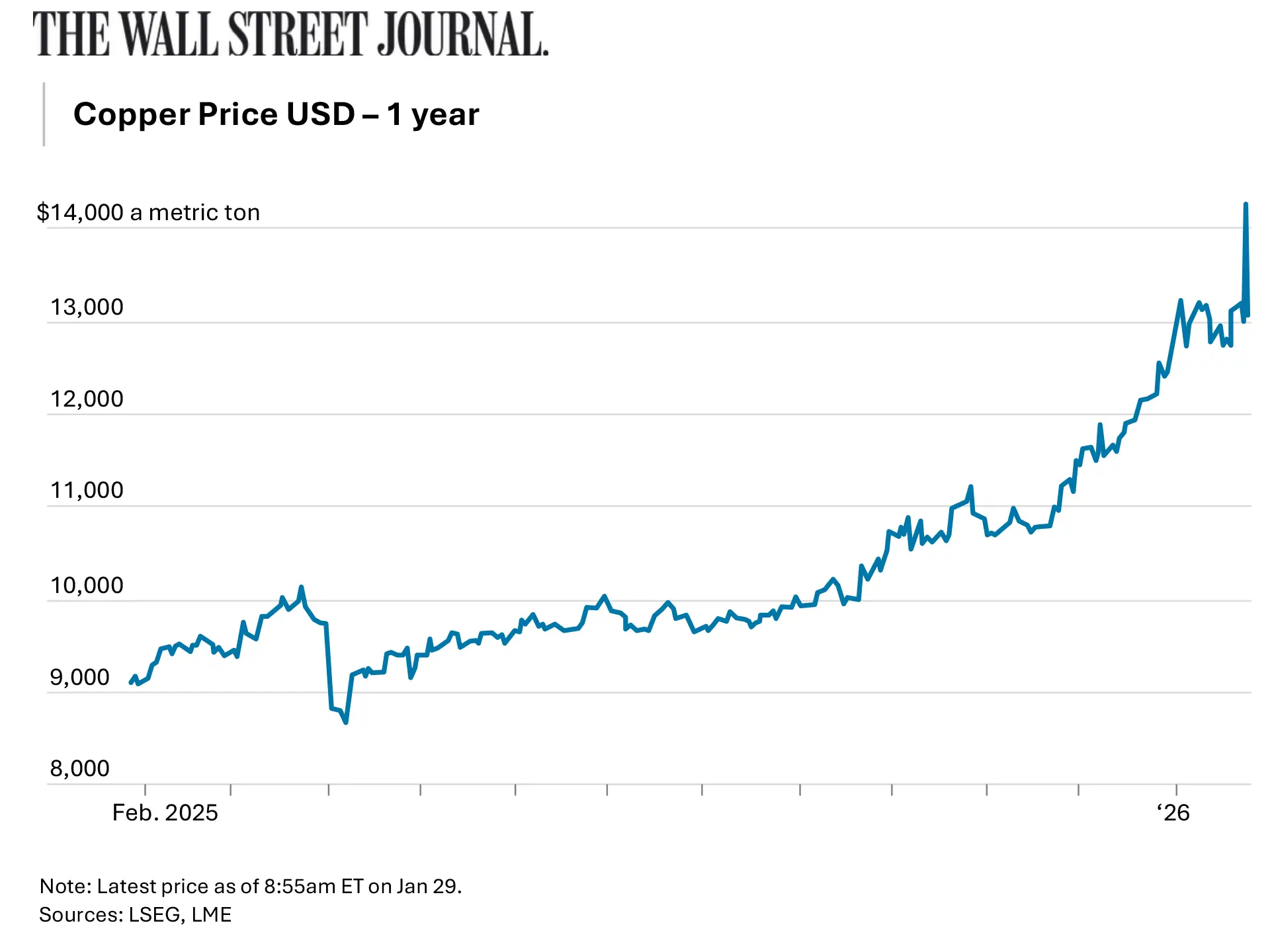

Global copper demand is projected to surge by 50% to 42 million metric tons by 2040, driven by electrification, AI data centers, and renewable energy, creating a potential 10 million tonne supply deficit by 2028.1

Wood Mackenzie warns “Insufficient mine investment could drive sustained shortages and price volatility.”2

Billionaire mining magnate Robert Friedland predicts a massive, long-term supply “train wreck”. He argued in 2024 that “copper prices must rise significantly—potentially to $15,000/tonne”3

Copper prices have surged to historic highs, exceeding $14,000 a tonne in late January 2026, driven by a massive intensifying supply constraints and decades of underinvestment in new mining projects.4

Historically a store of value in uncertain times. And uncertainty doesn’t even begin to describe current geopolitical instability.

The price has skyrocketed in the last few years, hitting record highs nearly every month, and despite volatility experts forecast continued record-breaking growth.

At current prices mining projects that were once deemed borderline economical may now be highly cost-effective.

Gold Jumps Back Above $5,000. The Precious Metals Rally Is Back

JPMorgan has raised its year-end 2026 gold price forecast to $6,300 an ounce, citing sustained and strengthening demand from both central banks and investors, even after the recent bout of sharp price volatility.

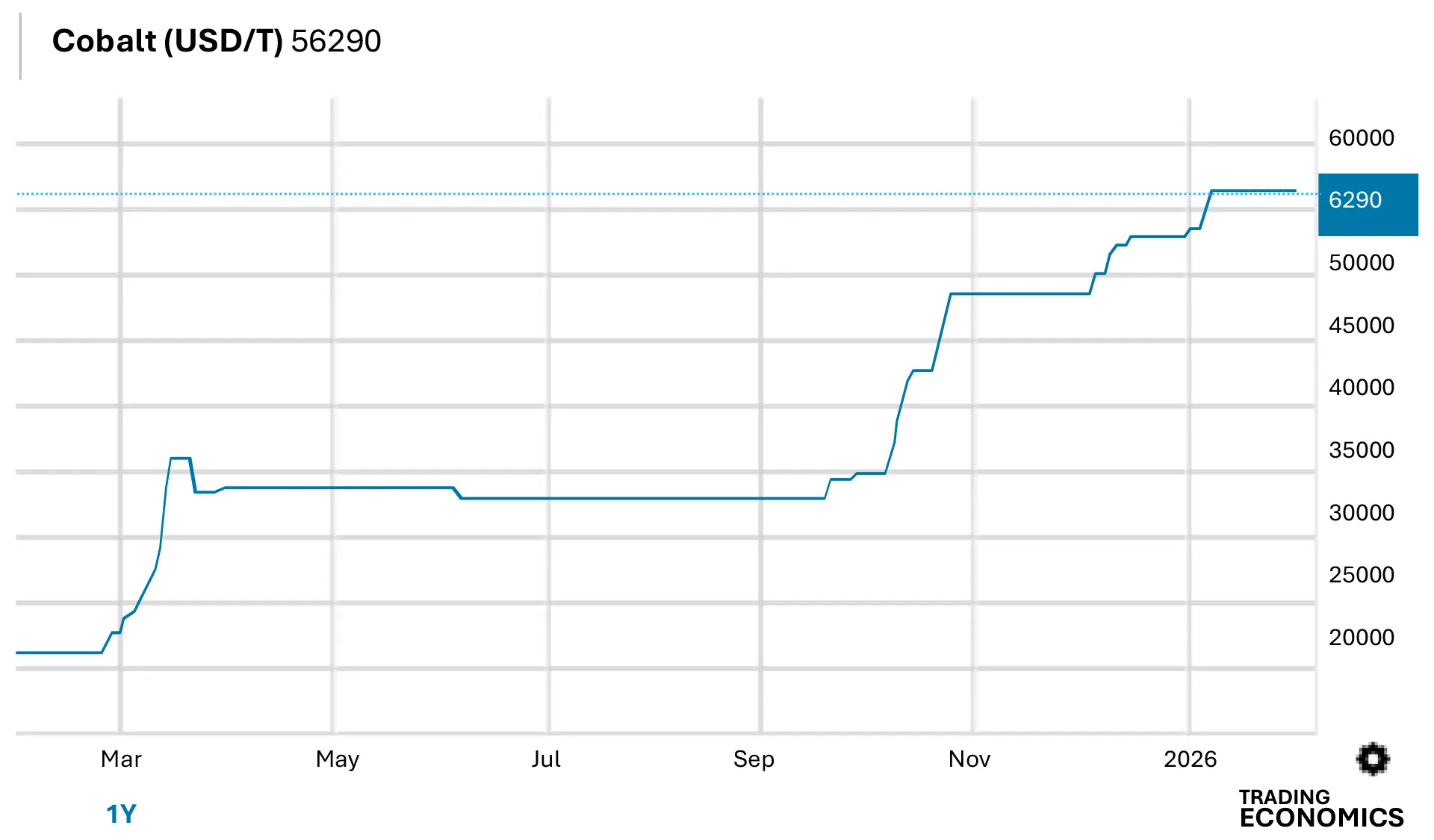

Global cobalt demand is projected to rise faster than supply over the next decade, potentially pushing the sector into deficit by the early 2030s.1

The global price of cobalt has more than doubled in just the last year, and forecasts point to continued rising prices. Unrest and export controls in the Democratic Republic of the Congo, the world’s leading cobalt supplier, has led to supply shortages.2

Cobalt’s crucial role in manufacturing EV batteries and superalloys is driving growing demand. Due to its critical nature, governments are building strategic reserves, with the U.S. seeking to procure up to 7,500 tons ($500M USD) of alloy-grade metal.3

The vast majority of the global Cobalt Supply is mined under atrocious working conditions, including both child, and slave labor. The profits from these Cobalt mines are often used to fund terrorism and war. Because of this, “Ethical Cobalt” sources, like Cobalt produced in Europe, often fetch premiums of ~10% above market prices.4